[SUMMARIES]

Evaluates the top 5 processors for SMEs: Stripe, HitPay, Airwallex, PayPal, and Adyen.

Highlights core differences in transaction fees, multi-currency support, and local methods (e.g., PayNow).

Notes the mandatory requirement for a Singapore corporate bank account to enable local gateway integration.

Explains how automating accounting data via gateways saves SMEs time, with Koobiz managing the process.

[/SUMMARIES]

Choosing the right platform when you pick top 5 payment gateways in Singapore for SMEs directly dictates your startup’s cash flow. Koobiz supports founders as they navigate this landscape, alongside our company incorporation services. This guide explains transaction fees, PayNow integration, corporate bank account requirements, and accounting automation to smoothly power a Singaporean venture.

What is a Payment Gateway and Why Do Singapore SMEs Need One?

Understanding the mechanism behind online payments is vital for any modern business transitioning into the digital space.

What is a Payment Gateway?

A payment gateway is a secure digital infrastructure acting as a bridge between an SME’s e-commerce website, the customer’s payment method, and the acquiring bank to authorize transactions. It essentially functions as the digital equivalent of a physical point-of-sale (POS) terminal. When a customer clicks “pay,” the gateway encrypts their sensitive details and securely transmits this data to process the sale.

Why Singapore SMEs Need It

For SMEs in Singapore, integrating a robust payment gateway is a fundamental operational requirement, not a luxury. Here’s why:

- PCI-DSS Compliance & Security: Automatically encrypts credit card data and mitigates fraud risks with advanced algorithms, safeguarding both you and your customers.

- Localized Payment Support: Enables instant acceptance of popular local methods like PayNow, GrabPay, and DBS PayLah!, reducing checkout friction.

- Automated Accounting & Compliance: Seamlessly routes funds into your corporate ledger and auto-syncs with accounting software—a streamlined process Koobiz helps optimize to ensure IRAS compliance.

Industry reports and merchant surveys show SMEs offering localized payment gateways typically see a 30–40% increase in checkout conversions versus those relying solely on manual bank transfers.

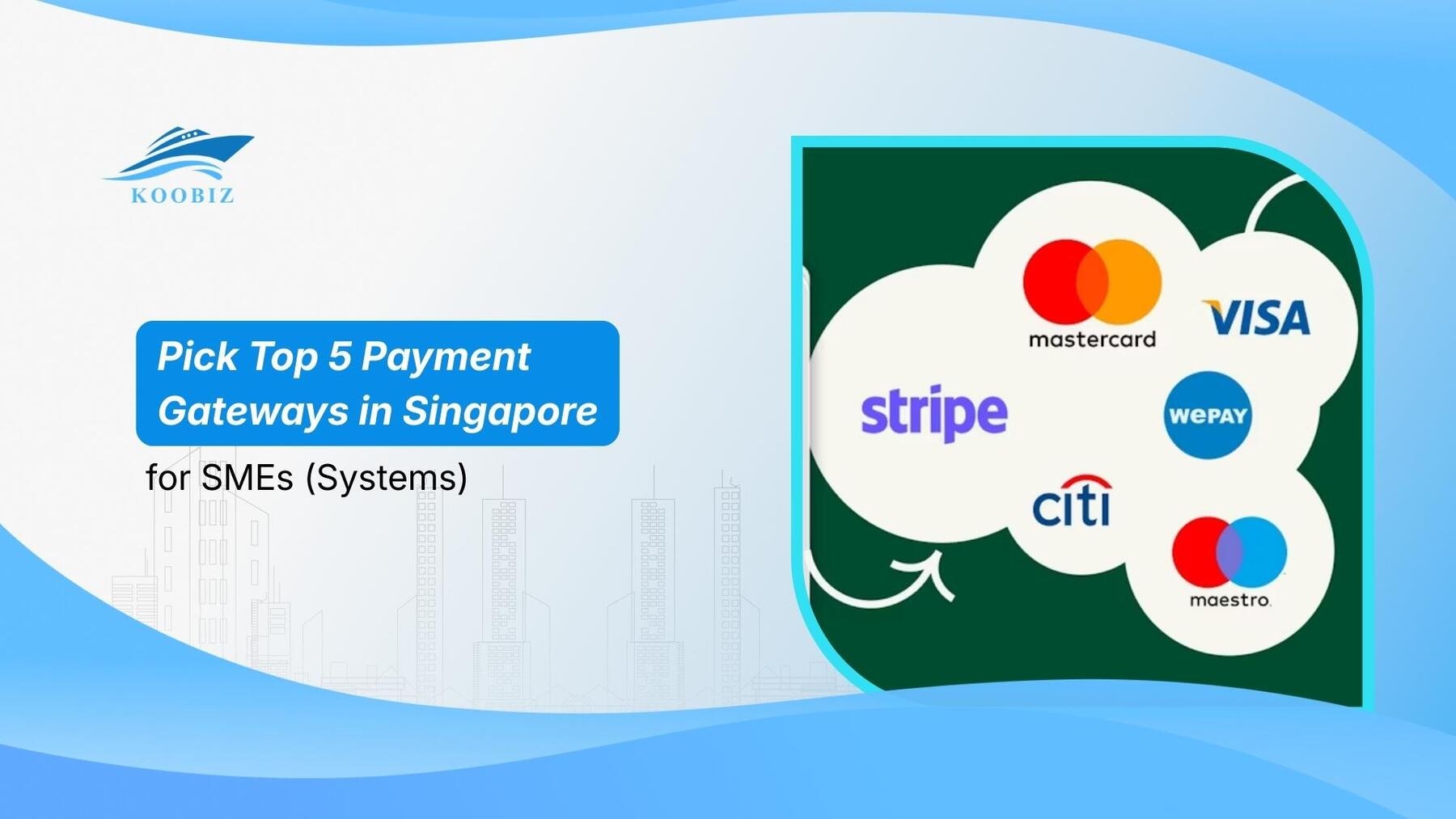

Top 5 Payment Gateways in Singapore for SMEs (2026 Review)

There are five leading payment gateways for SMEs in Singapore: Stripe, HitPay, Airwallex, PayPal, and Adyen. These platforms differ in transaction fees, payout times, and the local payment methods they support.

Next, we’ll explore the specific characteristics of each platform to help you identify the best fit for your business model.

| Payment Gateway | Standard Domestic Fee (Est.) | Standout Feature | Best For |

|---|---|---|---|

| 1. Stripe | 3.4% + $0.50 SGD | Advanced Developer APIs | Global E-commerce & SaaS |

| 2. HitPay | Very Low (via PayNow) | No-Code Local Integrations | Local Retail & Pop-ups |

| 3. Airwallex | Varies (Great for FX) | Zero Forced Conversion | Cross-Border/Importers |

| 4. PayPal | ~3.9% + Fixed Fee | High Global Brand Trust | Freelancers & Consultants |

| 5. Adyen | Interchange++ | Omnichannel Processing | Mid-Sized Retailers (Online/POS) |

Each of these systems provides unique advantages, depending on whether your primary customers are local or international, and on whether you need deep developer customization or a straightforward plug-and-play solution.

1. Best for E-commerce & Developer APIs: Stripe

Stripe remains the industry gold standard for businesses that require high customization and robust API integrations. It’s especially preferred by tech-savvy startups and comprehensive e-commerce stores using platforms like Shopify or WooCommerce.

- Transaction Fees: Typically 3.4% + SGD 0.50 per successful card charge, with volume-based discounts possible.

- Key Features: A powerful suite of developer tools, advanced fraud protection via Stripe Radar, and support for over 135 currencies.

- Best Fit: SMEs aiming to scale globally with a highly tailored checkout experience.

2. Best for Local Singapore Payments (No-Code): HitPay

HitPay is a homegrown solution tailored for Singaporean SMEs. It shines with no-code setup, making it especially accessible for merchants without an in-house tech team.

- Local Integration: Seamlessly supports PayNow, DBS PayLah!, GrabPay, and ShopeePay in addition to standard credit cards.

- Cost Efficiency: Delivers some of the lowest fees for local transactions; for example, PayNow fees are significantly cheaper than typical credit card processing rates.

- Best Fit: Ideal for retailers, pop-up stores, and service-based SMEs that primarily serve the domestic Singaporean market.

3. Best for Multi-Currency and Cross-Border SMEs: Airwallex

Airwallex is changing how SMEs manage international transactions by combining a payment gateway with strong FX and borderless account capabilities.

- Zero Forced Conversion: Unlike typical gateways, Airwallex lets you collect payments in multiple currencies and hold funds in foreign currency accounts without forced conversion. When you do convert, you can access highly competitive, near-interbank rates.

- Key Features: Includes virtual corporate cards and smooth global payout capabilities.

- Best Fit: E-commerce businesses that source from overseas or sell to international markets (e.g., US, UK, Australia) and want to minimize currency conversion fees.

4. Best for Global Trust and Fast Setup: PayPal

PayPal is universally recognized, offering an immediate sense of trust and security to buyers who might be hesitant to enter their card details on a new SME website.

- Ease of Use: Creating a PayPal business account is quick, making it a fast route to market for a brand-new entity.

- Consideration: Transaction fees (typically around 3.9% + a fixed fee for domestic transactions, higher for cross-border) and FX rates can be higher than some competitors.

- Best Fit: Freelancers, new consultants, or boutique e-commerce stores prioritizing buyer trust over the lowest transaction cost.

5. Best for Omnichannel Retailers: Adyen

Adyen is an enterprise-grade solution that has scaled down to accommodate growing SMEs, particularly those blending physical and digital commerce.

- Unified Commerce: One platform to manage online payments, in-app purchases, and in-store POS transactions.

- Data Insights: Rich analytics on shopper behavior across all sales channels.

- Best Fit: Mid-sized SMEs operating brick-and-mortar stores in Singapore while running high-volume online stores.

Stripe vs. HitPay vs. Airwallex: Which is Better for Your Singapore Startup?

Choosing between these top three contenders depends entirely on your startup’s primary operational focus. To illustrate further, here is a quick scenario-based breakdown:

- Choose Stripe if: Your startup needs a bespoke SaaS checkout embedded directly into your software, with world-class API docs and a robust developer ecosystem.

- Choose HitPay if: You’re a local bakery, boutique agency, or Instagram-based store in Singapore, and you want to generate PayNow QR codes instantly without coding.

- Choose Airwallex if: You’re a dropshipping startup or an agency with global freelancers; you need to collect USD from clients and pay suppliers in USD without SGD conversion, preserving margins.

Startups using multi-currency gateways like Airwallex can save an estimated 2–3% in total revenue by avoiding unnecessary FX markups and using like-for-like settlement.

Do All Payment Gateways in Singapore Require a Local Corporate Bank Account?

Yes, almost all reputable payment gateways in Singapore require a local corporate bank account.

Setting up the proper legal and financial structures is a critical first step before accepting online payments. Because payment gateways such as Stripe and HitPay operate under the strict regulations of the Monetary Authority of Singapore (MAS), they have a compliance obligation to ensure funds are disbursed securely. Therefore, they will only deposit earnings into a corporate bank account bearing the precise name of your incorporated business. This safeguard exists for three key reasons:

- ACRA & IRAS Compliance: Avoids routing business revenue to personal accounts, which can violate gateway terms and complicate taxes.

- Direct SGD Payouts: Enables smooth daily/weekly settlements without fund holds.

- Strict AML Standards: Banks and processors perform strict anti-money-laundering and identity checks before approving cash flow.

The process often involves stringent KYC and precise documentation, which can cause delays for foreign founders.

This is exactly where Koobiz steps in. Koobiz helps streamline company incorporation and guides you through opening a Singapore corporate bank account, preparing you to integrate with any payment gateway without delay.

Industry note: Surveys show many new businesses experience weeks of delays launching their digital storefronts due to incomplete corporate banking and KYC documentation.

How to Choose and Manage the Right Payment Processor for SMEs

Beyond simply accepting money, a top-tier payment gateway should optimize back-office operations. Choosing and managing processors means evaluating integration capabilities, transparent fee structures, and settlement speeds. Use this 3-step framework to treat your processor as an extension of your accounting department.

Step 1: Understand the Tech Stack (Gateways vs. Merchant Accounts)

A payment gateway captures and transmits payment data securely (the digital card reader). A merchant account is the bank account that actually receives and holds funds from card sales before settlement. Nowadays, aggregators like Stripe and PayPal offer a full-stack service, combining gateway technology and a shared merchant account, which greatly simplifies setup for SMEs.

Step 2: Evaluate the Hidden Costs and Settlement Speeds

Don’t rely solely on the lowest advertised transaction fee. Consider total cost of ownership. Assess hidden FX markups, chargeback fees, and, crucially, settlement speeds. A gateway that takes days to deposit funds can bottleneck cash flow, even if per-transaction fees are low.

Step 3: Automate Your Back Office (Xero/QuickBooks Integration)

Modern payment systems can auto-reconcile with cloud accounting software. Connect gateways like Stripe, HitPay, or Airwallex to Xero or QuickBooks to automatically log every transaction, including gateway fees. This level of integration reduces human error, keeps real-time P&L, and simplifies year-end tax filing. Koobiz can help: we design and implement these tech stacks to ensure your gateways talk seamlessly to your accounting software, so our tax professionals can provide accurate financial guidance and keep you IRAS-compliant.

Niche and Alternative Payment Solutions for Singapore Businesses

While the top options cover most needs, exploring alternatives is smart for specialized niches (e.g., crypto processing or high-risk underwriting). Singapore’s regulatory environment supports several specialized processors that may be more suitable than mainstream gateways.

Alternative Solutions for Crypto Payments

- The Challenge: Web3 payments can bring price volatility and MAS regulatory considerations.

- The Solution: Legally accepting cryptocurrency is possible and potentially profitable with a Major Payment Institution (MPI) licensed processor, such as Triple-A. These gateways convert crypto (e.g., Bitcoin, USDT) to fiat (SGD) at the point of sale, shielding you from volatility and reaching tech-savvy global customers.

Processing for High-Risk Sectors

- The Challenge: Businesses in “high-risk” categories (e.g., adult entertainment, certain gaming, vaping, or high-volume dropshipping with high chargeback risk) may find mainstream gateways freezing accounts.

- The Solution: SMEs in these niches may need specialized high-risk merchant accounts. These providers typically charge higher transaction fees and may require rolling reserves, but they offer the underwriting needed to keep payment acceptance open.

Accelerate Your Business Growth with Koobiz

Choosing the right payment gateway is only one piece of the puzzle. To build a highly profitable, legally compliant, and operationally efficient business in Singapore, you need a solid corporate foundation.

At Koobiz (koobiz.com), we are more than just a corporate secretary. We are your strategic partners in growth. From seamless Singapore company incorporation to expert guidance on opening your corporate bank account, we ensure you pass all KYC hurdles swiftly. Once your business is live, our elite tax, accounting, and auditing teams ensure your payment gateway data flows perfectly into your financial records, keeping you fully compliant with ACRA and IRAS.

Focus on making sales; let Koobiz handle the numbers. Visit us today to streamline your corporate journey!

")

to Alipay")

, 20 (≥90th percentile)")

vs. Excluded (NO)")

from Non-Profit Organizations (NPO)")