[SUMMARIES]

Mandatory Requirement: Changing a company name requires a Special Resolution, requires a Special Resolution with a minimum 75% majority vote from eligible shareholders.

The Platform: All applications must be submitted via the ACRA BizFile+ portal using CorpPass.

Cost & Time: The name application fee is SGD 15 (paid upfront). Standard approvals are often instant or take up to 3 days, but referral cases can take 14-60 days.

Post-Change Duties: You must update your company seal, bank accounts, and licenses. IRAS updates automatically, but CPF may require manual notification.

Name Restrictions: Proposed names must not be identical to existing entities, undesirable, or similar to reserved names.

[/SUMMARIES]

Rebranding or strategic shifts often require a new company name. However, beyond branding, renaming a business is a formal legal procedure governed by ACRA and the Singapore Companies Act. Success relies on precise compliance and documentation, specifically the passing of a Special Resolution.

Koobiz simplifies the entire rebranding journey, ensuring your transition remains compliant and rejection-free. Whether you are fixing a typo or launching a complete rebrand, following the correct procedure is vital to avoid rejection. This guide provides a clear walkthrough of the change company name Singapore process, from the initial BizFile+ reservation to drafting your Special Resolution and the essential steps to take after approval.

Pro Tip for Foreign Companies: If you are a branch of a foreign company, Critical Note for Branches: Ensure the parent company’s name is officially updated in its home jurisdiction before notifying ACRA.

Requirements for Changing Company Name in Singapore

To ensure a seamless transition and avoid immediate rejection, your company must meet four foundational legal requirements: Failing to meet these foundational elements often leads to immediate rejection, wasting both time and non-refundable filing fees.

1. Name Availability & Uniqueness

The first step is ensuring your proposed name strictly adheres to ACRA’s naming conventions to avoid being flagged as identical or phonetically similar. The proposed name cannot be identical to an existing entity, nor can it be phonetically similar to names already reserved.

- Uniqueness Check: You must conduct a thorough search on BizFile+ to ensure no other business uses the same name.

- Avoid Similarities: ACRA maintains strict standards; for example, adding ‘(Singapore)’ to an existing name will still result in a similarity rejection.

2. Shareholder Approval (Special Resolution)

Legally, a name change requires a formal update to the company’s constitution, which necessitates specific shareholder consent.Unlike minor administrative changes that directors can approve, a name change alters the company’s constitution.

- 75% Majority: You must pass a Special Resolution with a 75% supermajority vote from shareholders holding voting rights.

3. Avoid Restricted Words

Be mindful that restricted terms (e.g., ‘Bank’, ‘University’) often trigger mandatory referrals to agencies like MAS or MOE, extending the approval timeline.

- Restricted Terms: Words like “Bank,” “Insurance,” “University,” or “Education” require external approval.

- Undesirable Words: The name must not contain vulgarities or imply a connection to government bodies without permission.

4. Constitution Compliance

Finally, review your Company Constitution (formerly Articles of Association) for any internal clauses that may impose stricter requirements than the standard Companies Act.

- Check Clauses: Check your company’s Constitution (formerly Articles of Association) to see if there are additional clauses regarding name changes beyond the standard Companies Act requirements.

Step-by-Step Guide to Filing a Name Change on ACRA

Updating your corporate identity involves four critical stages, managed almost entirely through the ACRA BizFile+ portal.

Here is the detailed procedure to ensure a successful filing:

Step 1: Check, Reserve, and Pay for the New Name

The process begins with securing name approval. You must first submit a formal application to ensure the name is available and compliant. Log in to BizFile+ using your CorpPass credentials. Navigate to the “Start a Business” or “Local Company” section and select “Application for a New Company Name.”

- Application Fee: A non-refundable SGD 15 fee is payable to ACRA at this stage.

- Approval: If the name is available and requires no external approvals, it is often approved within minutes. Upon successful approval, the name will be exclusively reserved for your company for a period of 120 days.

Step 2: Convene an EGM and Pass the Resolution

With the name reserved, the next legal requirement is to convene an Extraordinary General Meeting (EGM) to formalize shareholder consent. During this meeting, the shareholders must vote on the name change. Expert Support: The Koobiz secretarial team specializes in drafting precise Minutes of Meeting and Special Resolutions to ensure your name change is legally airtight.

Step 3: File “Change in Company Information”

Once the resolution is passed, finalize the process by submitting the ‘Change in Company Information’ filing on BizFile+.

- Select “File eServices” > “Local Company” > “Make Changes” > “Change in Company Information”.

- Select “Change in Company Name”.

- Enter the Transaction Number of the approved name application from Step 1.

- Mandatory Attachment: You are required to upload the signed Special Resolution (in PDF format) as evidentiary proof for ACRA.

Step 4: Final Endorsement

Once the transaction details are finalized, the application must be endorsed by the directors or a Registered Filing Agent (RFA) like Koobiz. Upon successful submission, ACRA will process the request. Upon ACRA’s approval, you will receive a formal email notification containing the Notice of Incorporation under New Name, confirming the change in the public register.

What is a Special Resolution for Name Change?

A Special Resolution is a high-level corporate decision necessitating at least 75% shareholder approval—a threshold significantly higher than standard ordinary resolutions. As renaming a company effectively alters its Constitution and identity, Section 28 of the Companies Act mandates this strict level of consensus.

To ensure the resolution is legally valid, you must adhere to the following protocols:

- Voting Threshold: You must obtain a majority of at least 75% of the total voting rights from shareholders present and voting at the meeting.

- Notice Period: A formal written notice must be served 14 days in advance for private companies (21 days for public entities), clearly stating the intent to pass a Special Resolution.

- Short Notice Exception: An EGM can be convened on shorter notice provided shareholders holding at least 95% of the total voting rights provide their consent.

- Written Resolution Option: To streamline the process, SMEs may bypass physical meetings by circulating a Written Resolution, provided it is signed by all eligible shareholders.

Koobiz Advice: Always retain the signed resolution in your Minute Book. This document serves as definitive proof of compliance during statutory audits or potential shareholder disputes.

Processing Time and Fees for Name Change Application

The core fee is SGD 15 (paid during the name application in Step 1).

- Understanding Approval Timelines: Approval times vary significantly based on your chosen name:Comparing the scenarios helps manage expectations:

- Standard Application (Instant): For a unique name with no restricted words (e.g., changing “ABC Trading Pte Ltd” to “XYZ Logistics Pte Ltd”), approval is often instant (15–20 minutes) or within one working day.

- Referral Application (Delayed): If your new name includes regulated words like “Architecture,” “Law,” “Hospital,” or “Estate,” the application is routed to the respective government body.For names requiring agency referral, expect a processing window of 14 days to 2 months.

Important Note: The SGD 15 filing fee is non-refundable. Any rejection will require a fresh application and a new fee payment.

Post-Approval Checklist: What to Do After Changing Company Name?

Securing ACRA’s approval is a major milestone, but you must now update your operational records to prevent compliance breaches.

Here are the five critical areas to update immediately:

Corporate Bank Accounts: This is urgent. Submit your ACRA Business Profile and Certificate of Change of Name to your bank.

Urgent: Update your corporate bank account details immediately. Cheques issued under the former name may be dishonoured after a brief grace period.

Government Licenses & Permits: Notify agencies like SFA (food) or STB (travel) immediately. While ACRA updates the central registry, specific licenses.

Action Required for CPF: Unlike IRAS, which syncs weekly, CPF contributions often require manual notification via your updated Business Profile.

CPF and IRAS:

- IRAS: Generally updates automatically on a weekly basis based on ACRA records.

- CPF: Often requires manual notification. You may need to send them your updated ACRA Business Profile to ensure contributions continue smoothly.

Company Seal and Rubber Stamp: Order a new Company Seal and rubber stamp with the new name and UEN. Ensure a new Company Seal and rubber stamp are produced immediately; using outdated stamps can jeopardize the validity of legal contracts.

Stationery and Digital Presence: Update your letterheads, invoices, website, email signatures, and signage. The Companies Act requires your correct name and UEN on all official correspondence.

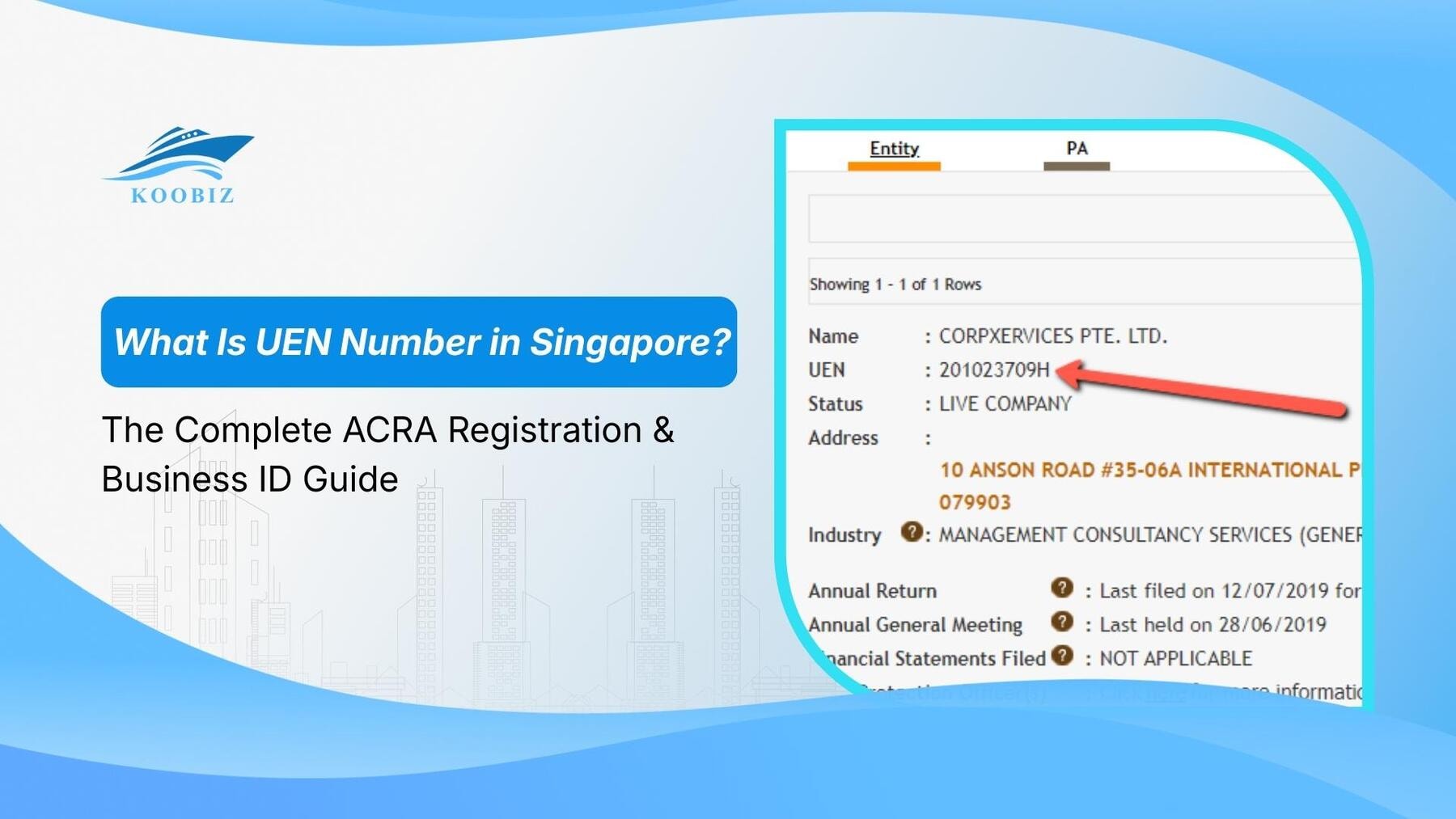

Does the UEN Change When the Company Name Changes?

UEN Continuity: Your Unique Entity Number (UEN) remains unchanged throughout the company’s lifespan, regardless of any name changes.

The UEN is a permanent ID issued at incorporation. It stays with the company until dissolution, regardless of name changes. This ensures business continuity, allowing you to reassure suppliers and clients that the legal entity they are contracting with remains the same.

Why Does ACRA Reject Name Applications?

While the process is straightforward, ACRA maintains strict oversight. Rejections typically stem from three primary non-compliance areas:

- Identical Name Conflicts: ACRA’s algorithm disregards common identifiers such as ‘The’, ‘Pte’, or ‘Ltd’. Therefore, ‘Best Tech Pte Ltd’ is legally viewed as identical to ‘Best Tech Ltd’.

- Prohibited & Undesirable Terms: Any proposed name deemed offensive, vulgar, or implying an unauthorized government connection (e.g., ‘Temasek’, ‘Asean’) will be summarily rejected.

- Pre-existing Reservations: You cannot claim a name already secured by another entity. Remember, a name reservation is legally valid for 120 days, even before incorporation is finalized.

The Koobiz Advantage: We conduct a comprehensive pre-clearance check against ACRA’s database to proactively mitigate rejection risks and save you unnecessary filing fees.

Difference Between Trading Name vs. Registered Company Name

Your Registered Company Name serves as your official legal identity, whereas a Trading Name (or Business Name) acts as a functional brand alias for marketing purposes.

| Feature | Registered Company Name | Trading Name (Business Name) |

|---|---|---|

| Legal Status | The official name approved by ACRA (e.g., “Koobiz Services Pte. Ltd.”). | An operational alias (e.g., ‘Koobiz Consulting’). Crucially, this must be registered with ACRA as a ‘Business Name’ and linked directly to your UEN. |

| Usage | Mandatory on invoices, contracts, and regulatory filings. | Used for signage and marketing, widely used for signage and branding; however, all statutory documents (contracts, invoices) must clearly disclose the underlying Registered Company Name to remain compliant. |

| Key Distinction | Legally protected in Singapore against identical registrations. | Provides the flexibility for a single entity to manage multiple brands without the administrative cost of forming separate subsidiaries. |

About Koobiz

Executing a successful name change in Singapore demands more than just a new brand vision—it requires meticulous corporate secretarial precision. At Koobiz (koobiz.com), Koobiz streamlines your entire compliance journey, from drafting legally airtight Special Resolutions to managing complex ACRA filings and banking updates.

Whether you need help with Singapore company incorporation, corporate bank accounts, or tax and accounting, partner with Koobiz for seamless growth. Let our experts handle the regulatory complexities while you focus on scaling your business in Singapore.

of Koobiz")

")

VS. NRIC (National Registration Identity Card)")

")

")

")